Stripe vs. Adyen: Collision Course

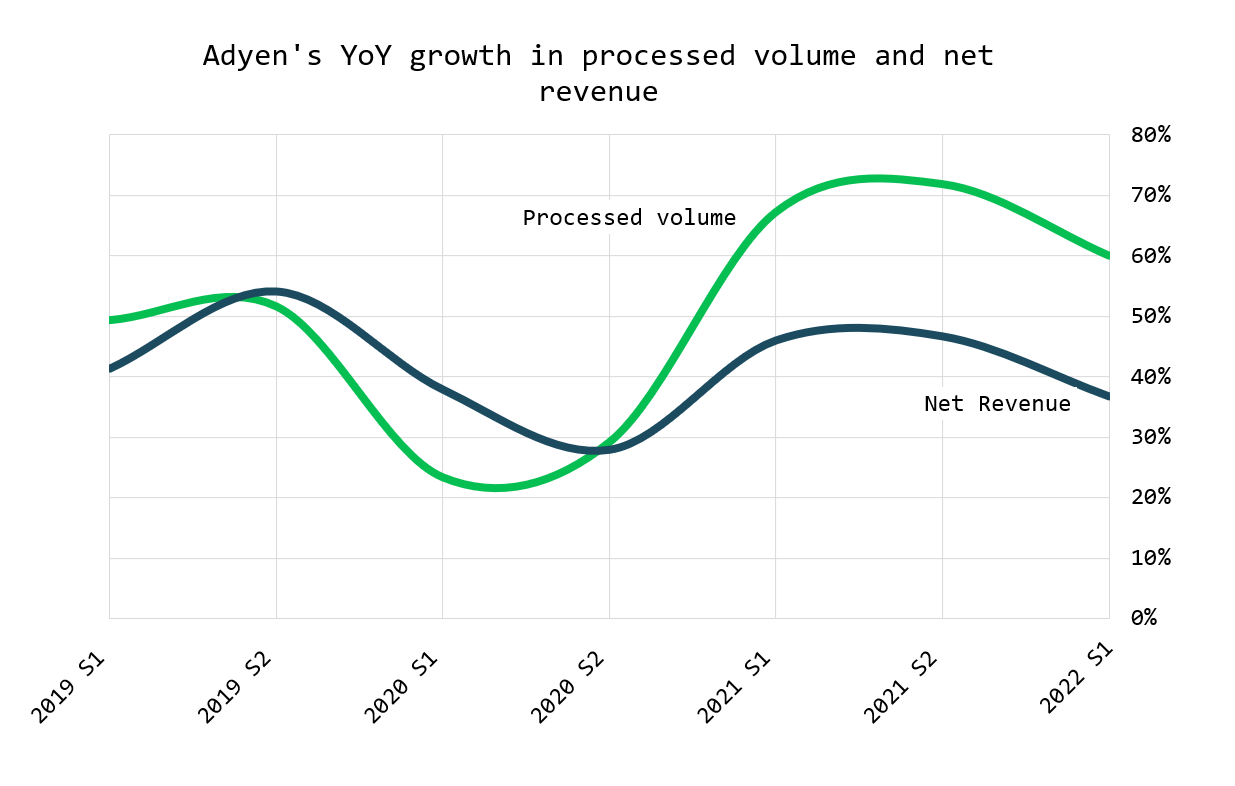

Adyen reported earnings last week and the company showed its usual strong growth with processed volumes up 60 percent year-over-year to €346 billion. This figure is the amount of money that is “swiped” through Adyen’s payment processing facilities. From processed volume, Adyen charges a fixed processing fee plus a fee determined by the payment method. This is Adyen’s gross “take rate” on processed volumes and it came to 114 basis points of processed volumes in the most recent half-year.

From this gross take rate, Adyen must pass cuts to all other financial intermediaries including Visa and Mastercard. What it’s left with is “net revenue,” from which we can derive a net take rate of 17.6 basis points in the most recent report.

This net take rate was substantially lower than the 20.6 basis points from the previous year, which is why Adyen’s net revenues grew only 37 percent despite the 60 percent increase in processed volumes:

In the earnings call, Adyen’s Ethan Tandowsky explained that Adyen has very little control over the gross take rate as this is mostly related to the payment methods used. And the company does not manage to net take rates: these are expected to decline: “If the merchant grows, we have lower pricing per transaction and therefore a lower take rate,” CFO Ingo Uytdehaage explained.

The other factor impacting net take rates was the increase in travel revenue. Because Adyen is not a full stack processor in travel—replaces fewer middlemen—it gets paid less per transaction.

We see both effects in the charts below. Take rates have declined as merchants have grown on Adyen (80 percent of the company’s growth comes from existing customers), and the spike in take rates in the first half of 2020 was from when travel was shut down. This resulted in fewer travel volumes and thus proportionately higher full stack take rates:

This decline in net take rate can be seen as a good or a bad thing, depending on how one looks at it.

The Good

The good thing about a declining take rate is that it lowers the risk of new entrants. The lower Adyen’s take rate, the greater the volume hurdle any new entrant must overcome to make money.

The Bad

A declining take rate is a sign that Adyen is increasingly servicing its core, upmarket enterprise customers. This leaves the lower end of SMBs vulnerable to new entrants. Leaving the lower end of the market open to a competitor can be very dangerous: in Clay Christensen’s original theory of disruptive innovation, new entrants at the low-end of the market show up with an inferior product. The incumbent is happy to retreat and serve its most profitable customers. Over time, the entrant’s solution becomes better, and it moves up market, eventually taking over the incumbent’s business. This is disruption.

But the empire is striking back. Here is FIS’s CEO Gary Norcross in June of last year, when asked about whether Stripe and Adyen are taking market share away from them:

Yes. Honestly, we don't see Stripe. Stripe tends to be down in the startup realm. And I mean if you ask me for a gap in our capabilities, we're not down in the very low end and then the startups on merchants or in the really small SMBs. That's actually an opportunity for us when you look at some of the stuff that we've now done with NAP and Access Worldpay. So we'll start pushing down in market, and I'm sure we'll see them more.

On global eComm, we really just run into Chase and we run into Adyen. We've made several announcements over the last several quarters of actually taking market share from Adyen and Chase. And so we feel good about where we're positioned. Our business grows just as fast or faster, depending on the market industry segments we're in. Once again, we've got -- travel and airlines has been a significant headwind for us in 2020. But as that recovers, it's going to be a very nice tailwind for us in 2021. Frankly, into 2022, that will continue to accelerate that growth.

The incumbents, particularly FIS and Fiserv, are also increasingly offering APIs for developers to build adjacent financial services. This appeals to startups. But Adyen must contend with something a lot more powerful than a new entrant or incumbents: Stripe.

Stripe vs. Adyen

Adyen was founded in 2006. Stripe was founded in 2010. Despite the four-year lead, Stripe has now surpassed Adyen in payment volumes and revenues. There are plenty of good articles on the origins of Stripe, so we won’t recap that history here. Adyen became a public company in mid-2018 and Stripe in 2020 hired the ex-CFO of General Motors, possibly in preparation for an IPO.

Whereas Adyen focuses on enterprise customers, Stripe focuses on startups and small businesses. In its recent Stripe Sessions event the company noted that 60 percent of tech companies that went public in 2021 are building on Stripe.

But Stripe’s SMB focus is widening. Stripe called out large enterprises that are now using its platform (besides the obvious, Shopify, which built its business on Stripe and probably gets a special deal with below-average take rates). Stripe co-founder John Collison, posing in front of the headquarters of automaker Ford, noted:

Over the last couple of years, enterprises have leaned on Stripe to achieve that. H&M introduced virtual fittings and a marketplace for used clothing. Le Monde, the great French newspaper, is now publishing an English-language online edition.

And here at Ford, they are starting to use Stripe Connect to build direct relationships with consumers and facilitate sales between consumers and dealerships.

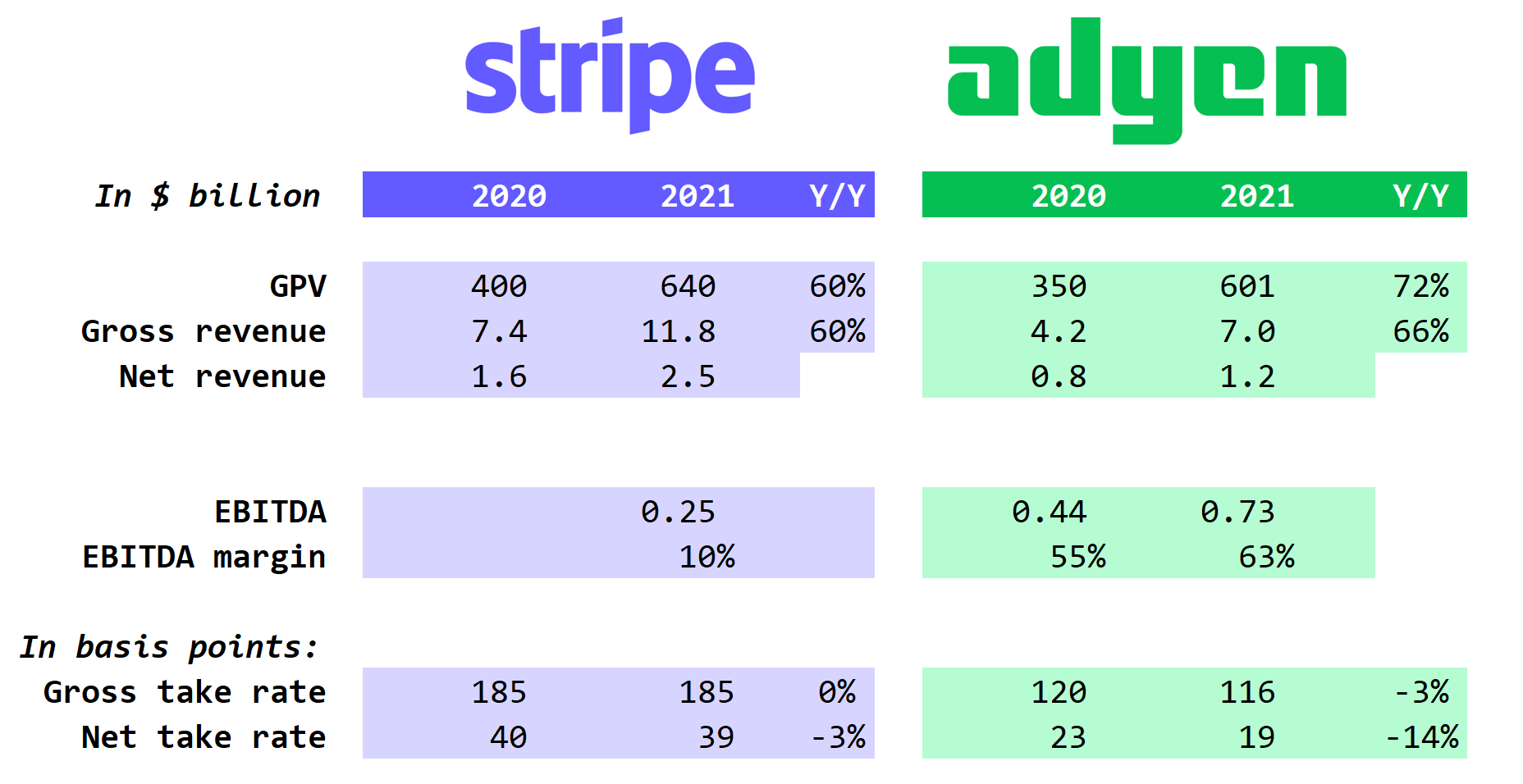

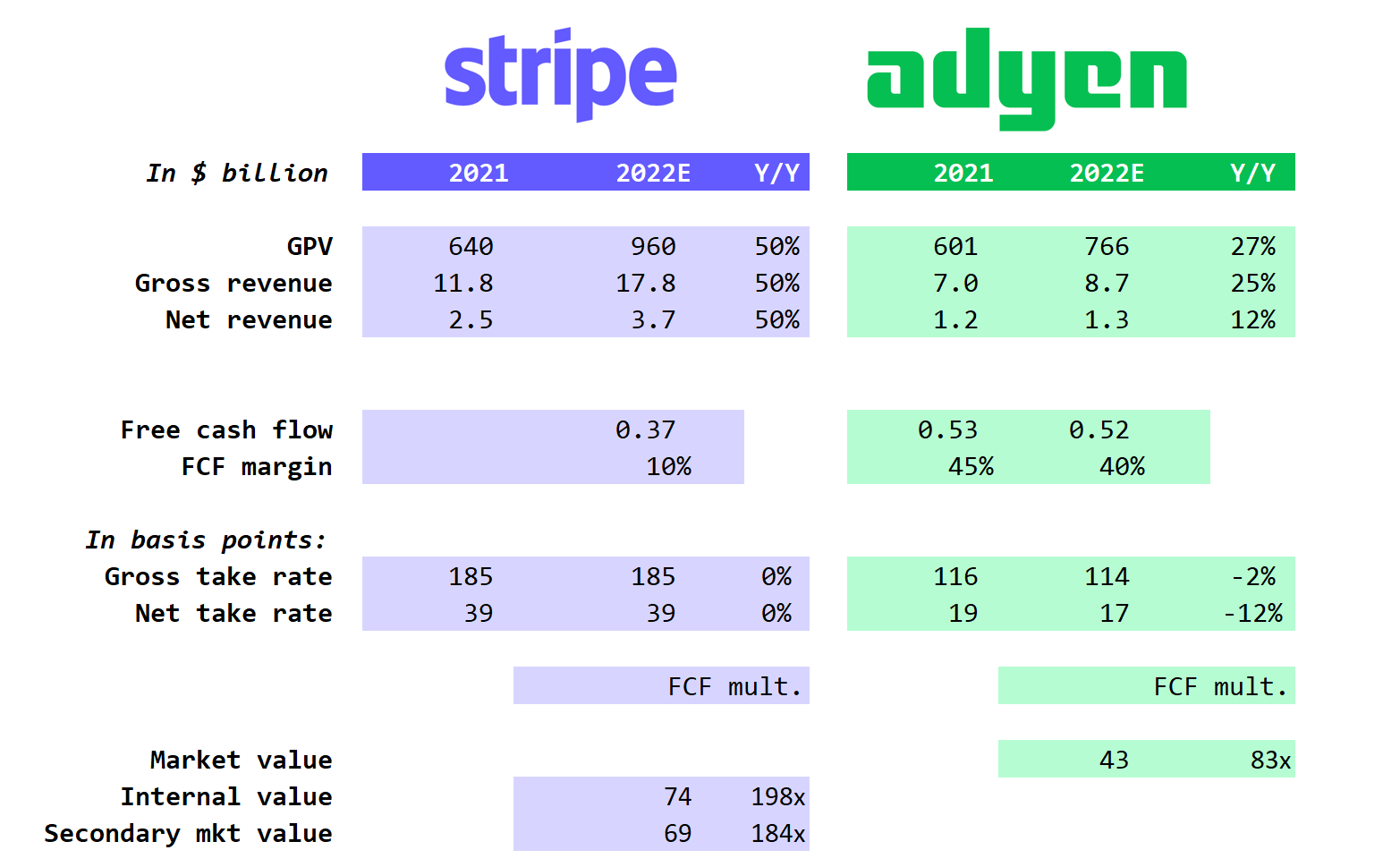

Because Stripe isn’t public, we don’t have access to its financials. However, recent reports by the WSJ and Forbes allow us to triangulate some of Stripe’s financials. The format was inspired by a previous analysis by Tanay Jaipuria.

The numbers below are taken from those two articles for Stripe, and from Adyen’s filings. They are adjusted to USD (since Adyen reports in EUR) using the average exchange rates for each year.

Between 2020 and 2021, Adyen grew faster than Stripe, with 72 percent growth in payment volumes and 66 percent growth in gross revenue. The erosion in Adyen’s take rate however resulted in lower net revenue growth.

We don’t know what Stripe’s EBITDA margin is, but reports calling it “hundreds of millions” probably means about 10 percent which would mean $250 million of EBITDA in 2021.

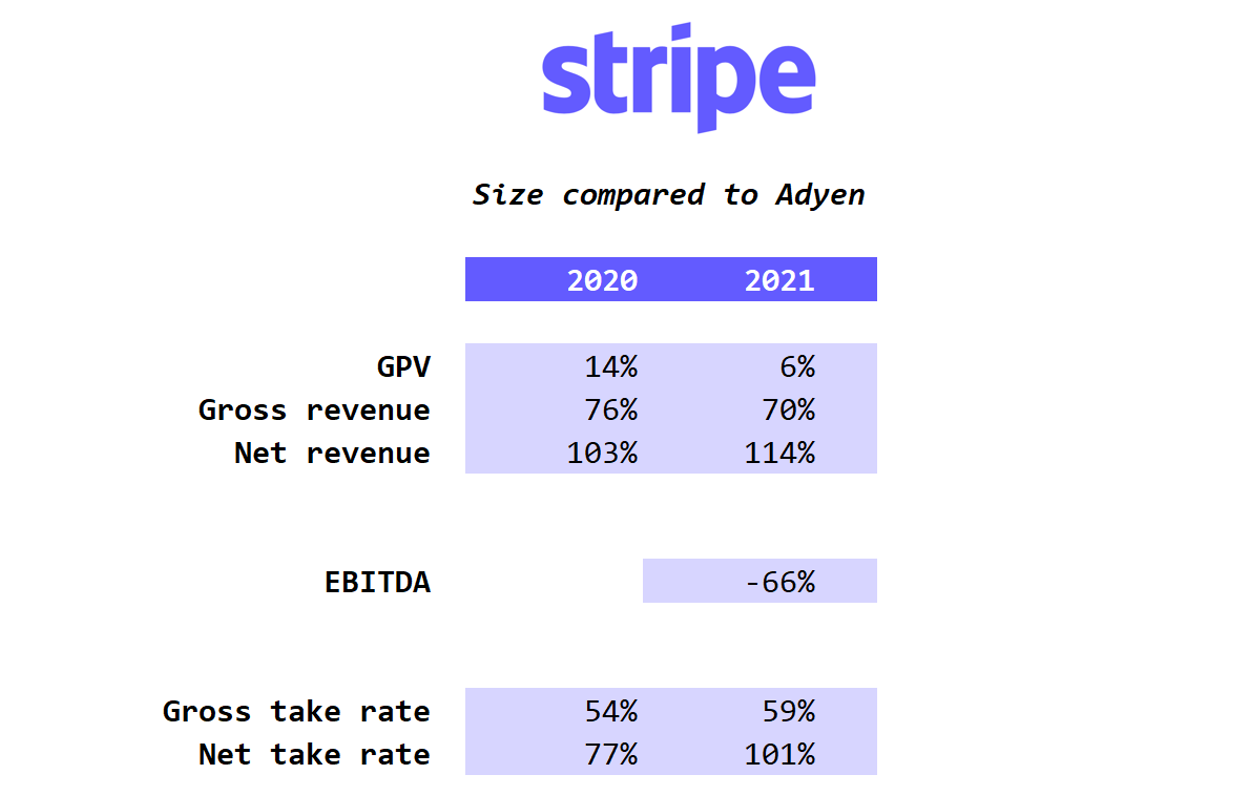

If this is the case, Adyen is significantly more profitable than Stripe. Although Stripe is slightly larger than Adyen on a processed volume basis, it captures significantly more revenues since it focuses on small companies and has higher take rates (39 basis points compared to 19 basis points for Adyen, or 2x Adyen’s net revenue take rate in 2021). Despite this, Adyen’s EBITDA is likely greater than Stripe’s.

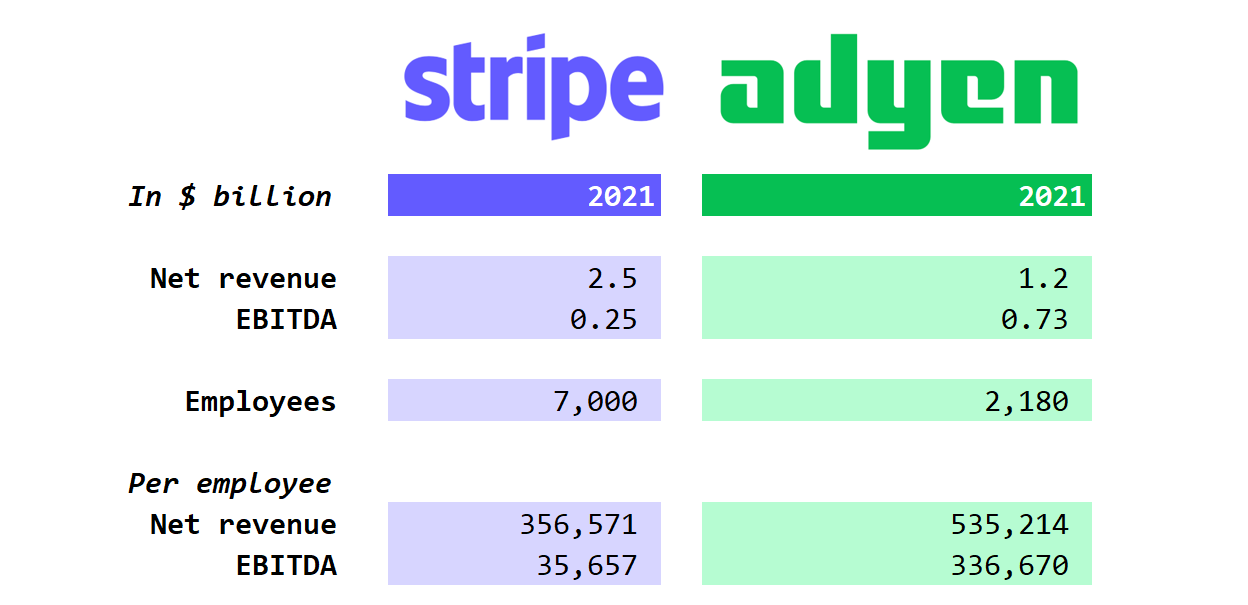

The reason is headcount: Stripe is reported to have around 7,000 employees, many of them in high-cost Bay Area, whereas Adyen finished 2021 with only 2,180 employees, 10 percent of them in the Bay Area.

If the 10 percent EBITDA margin estimate for Stripe is roughly right, this means Adyen is 9x more profitable in terms of EBITDA per employee:

Competitive Pressures – Adyen’s Margins

Adyen reported 59 percent EBITDA margins in last week’s earnings, compared with 61 percent in the year-ago period and the company’s long-term “above 65 percent” guidance. Most of this was related to hiring an additional 395 team members in the period. And the company is not stopping there: it highlighted the need to keep hiring, and keep burdening its EBITDA margins as a result, so that it can “design the next phase of Adyen for scale.”

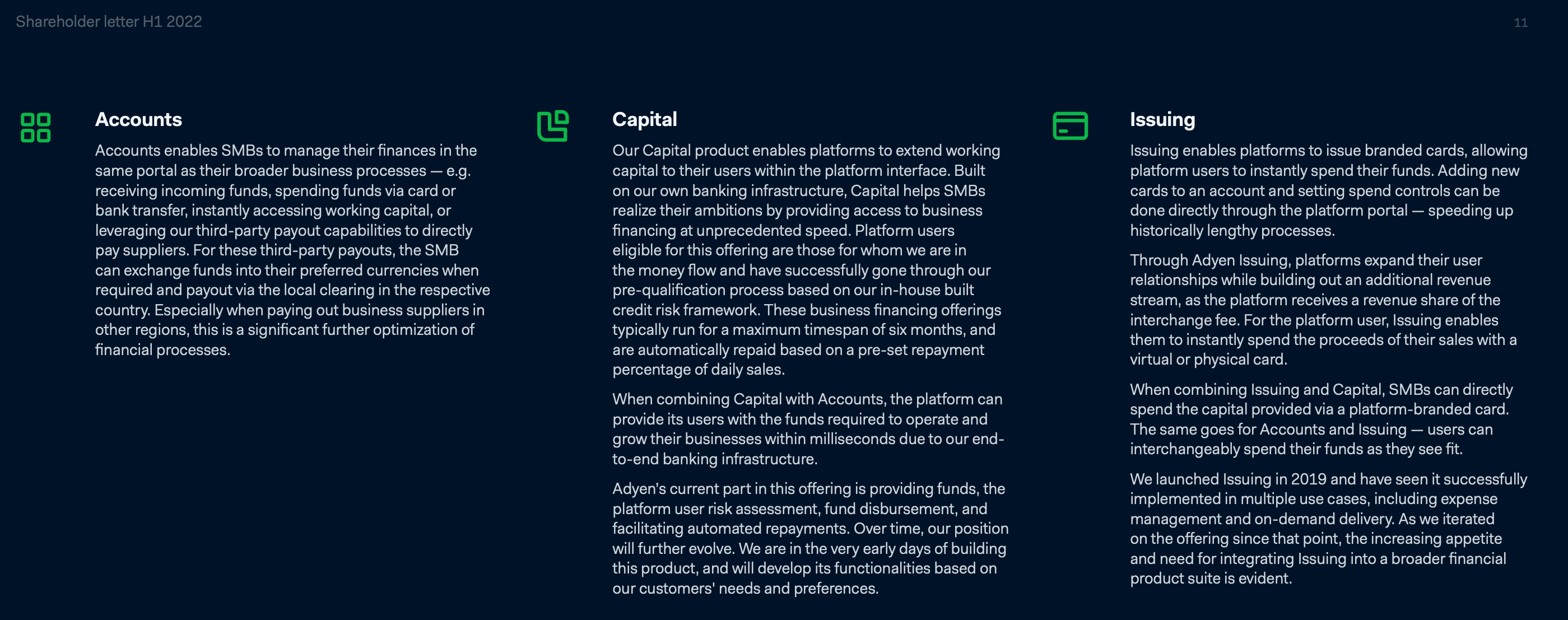

In slides accompanying the earnings report, Adyen noted “The under serving of SMBs by traditional financial institutions opens growth avenues for platform businesses and Adyen alike.” It also noted it will pursue “Banking as a Service” and included this slide showing a few pieces the company has already developed:

The mention of SMBs, additional hiring and the focus on software adjacent to payments (Accounts, Capital, and Issuing, so far) is a sign that Adyen is going increasingly head-to-head against Stripe, not to mention reinvigorated incumbents like FIS and Fiserv, or newcomers like Checkout.com. And, as we noted above, Stripe’s mention of enterprise customers means it’s moving upmarket and into Adyen’s territory.

My guess is that this is the last we’ll see of Adyen’s ~65 percent plus EBITDA margins for a while. If the company is truly going to tackle Stripe head on, it’s going to take a lot of investment.

Adyen is massively profitable and generated about $520 million of free cash flow in the last twelve months, a 45 percent margin on net revenues. If Adyen were to hire an extra 4,425 employees so it can reach Stripe’s scale, it would cost the company about $500 million in salary and wages at an estimated $120k per employee (which is a bit more than what Adyen spends per employee today). That would zero out its free cash flow for the year.

Stripe Sessions

Stripe Sessions was held in late May, and Adyen reported in late August. I don’t think it’s a coincidence that Adyen talked about Banking as a Service and their custom point of sale terminals. Here’s John Collison, co-founder of Stripe:

And Stripe’s POS:

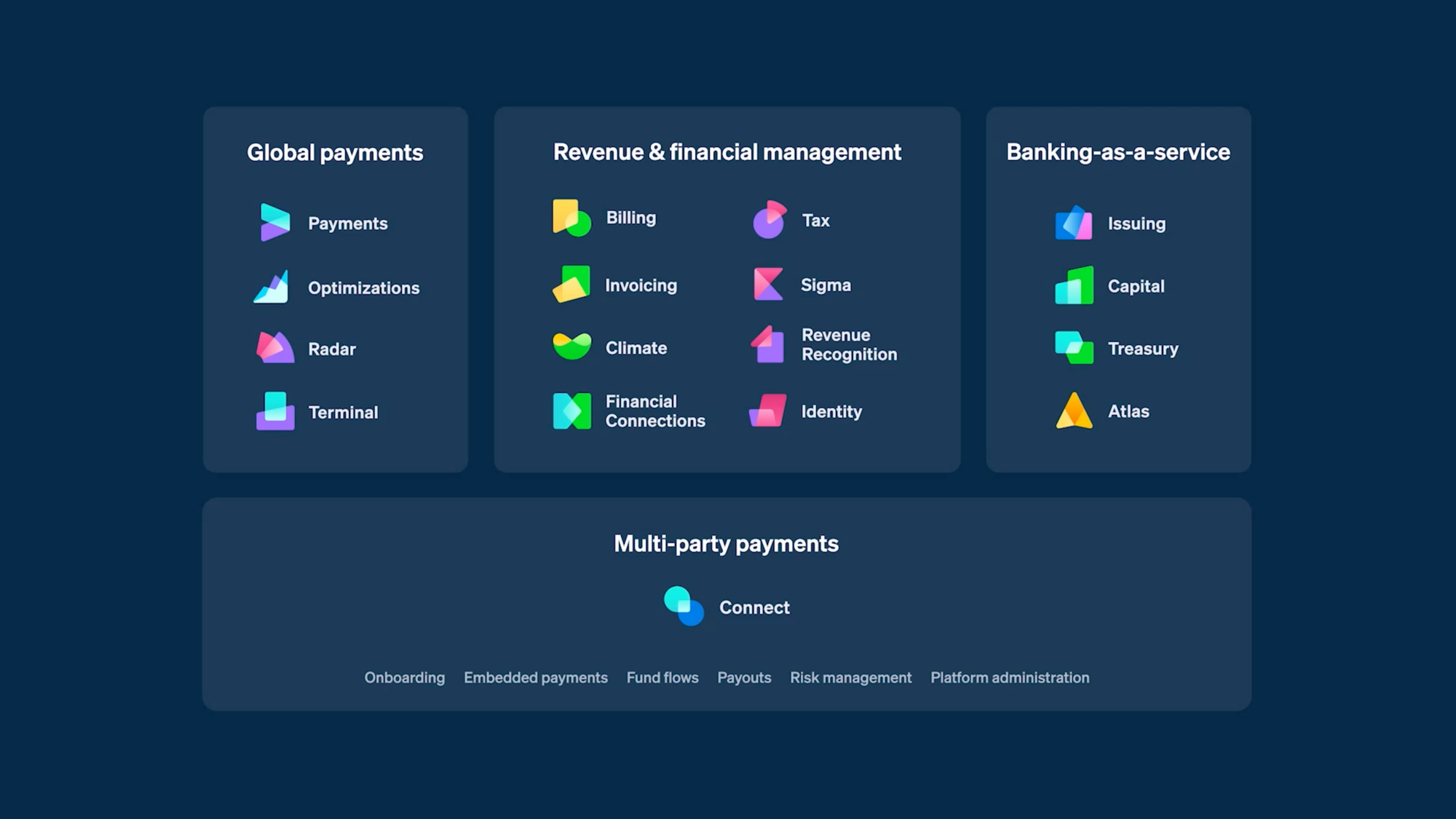

And this is why Adyen will need a lot more investment if it’s going to catch up: Stripe is way ahead in building all the Lego bricks for banking and related services:

Investing in Adyen and Stripe

The problem with Adyen’s high margins isn’t their level, of course, but rather, it’s the company’s valuation. With an enterprise value of $43 billion (now that the Euro has reached parity, we can ignore exchange rates) and $520 million in free cash flow, the company is valued at 83x this year’s free cash flow (or about 61x my estimate of forward free cash flow). That multiple might work, but it requires a long period of very high growth and sustained margins. With declining take rates and lower margins from required investments, this is not an easy bet to make.

Stripe famously does not allow trading in its shares, so various SPVs have sprung up to invest in Stripe through forward contracts with holders of shares. I’m told that Stripe’s shares in mid-2021, before the correction, reached a valuation of about $148 billion.

Today, the secondary market appears to have corrected to a valuation of about $69 billion, in the neighborhood of Stripe's own $74 billion internal valuation.

As we saw above, Stripe is not growing materially faster than Adyen. We don’t know how Stripe’s first half went (only that growth in 2022 is expected to be lower than 2021), but we do know it is less profitable than Adyen.

Adyen generated $730 million of EBITDA last year, and we estimated Stripe’s EBITDA at $250 million. Yet Stripe’s valuation in the secondary markets appears to be 60 percent greater than Adyen's ($69 billion compared to $43 billion).

My gut feeling is that the hype and secrecy around Stripe—and the lack of financials—pushes up the value of the company beyond what would be reasonable, even in this market correction.

Stripe at Adyen's free cash flow margins of 40 percent would generate about $1.7 billion of free cash flow this year, so it would be trading at about 40x free cash flow. This is reasonable, given Stripe's likely sustained growth ahead.

But it's highly unlikely that Stripe is anywhere near that margin, given reports that it generated "hundreds of millions" of EBITDA last year. We also know that Stripe has a large Bay Area workforce and is investing heavily for growth. My bet would be that after deducting stock-based compensation, Stripe probably generates no free cash flow.

Even if we granted Stripe a 10 percent free cash flow margin, it would be trading at nearly 200x free cash flow on its internal $74 billion valuation:

Note the decline in growth rate from Adyen stems from the effect of multiplying its Euro revenue in 2021 by about 1.16 (the exchange rate) and by 1 in 2022, with parity. Nominal growth reported in Euro will be more robust.

Still, these are rich valuations given the heightened competition, uncertain payoff of growth investments, and growth inflecting lower. Waiting for a better price doesn’t seem like a bad idea.